We’ve all felt it. That sudden, sinking feeling in the pit of your stomach when the check engine light comes on, a tooth starts to ache, or an unexpected email from your landlord announces a rent increase. It’s the anxiety of the unknown, the fear that one small setback could spiral into a major financial crisis.

What if you could replace that fear with a sense of security and control?

That’s exactly what an emergency fund does. Think of it as your personal financial safety net—a dedicated pool of cash that protects you from life’s inevitable surprises. It’s the buffer that stands between you and high-interest credit card debt when things go wrong.

If you’re starting from zero, the idea of saving hundreds or thousands of dollars can feel overwhelming. But it doesn’t have to be. This guide will give you a simple, step-by-step plan to build your emergency fund from scratch, showing you exactly how much you need, where to keep it, and how to start today.

What Is an Emergency Fund (And What Isn’t It?)

Before we start building, let’s be crystal clear on what we’re creating. An emergency fund is a stash of money set aside only for true, unexpected emergencies. It’s your “break glass in case of emergency” money.

The most important rule is that your emergency fund has one job: to be there when you need it. This means it is not:

- An investment fund: You don’t put this money in the stock market hoping it will grow. Its value must be stable.

- A vacation fund: That trip to the beach is a planned expense, not an emergency.

- A down payment fund: Saving for a house or car is a fantastic goal, but it needs its own separate account.

- A “sale at my favorite store” fund: This is for needs, not wants.

Think of it like a fire extinguisher for your finances. You hope you never have to use it, but you sleep a lot better knowing it’s there, ready to put out a financial fire before it burns down your whole house.

How Much Should You Have in Your Emergency Fund?

This is the number one question people ask, and the answer has two parts. The big, long-term goal and the small, immediate goal.

The Golden Rule – 3 to 6 Months of Essential Expenses

The standard advice from financial experts is to save enough money to cover 3 to 6 months of your essential living expenses. This is the amount you’d need to survive if you lost your primary source of income.

- Who needs 3 months? Households with stable jobs and multiple sources of income.

- Who needs 6+ months? Households with a single income, freelancers, commission-based workers, or anyone with a less predictable income stream.

But looking at that big number can be paralyzing. Don’t focus on it yet. Instead, focus on the most important first step.

The Most Important First Step – Your Starter Emergency Fund

Before you worry about six months of expenses, your only mission is to reach your starter emergency fund goal of $1,000.

Why $1,000? Because it’s an amount that’s large enough to cover most common emergencies—a car repair, a dental bill, an insurance deductible—but small enough to feel achievable. Hitting this first goal builds incredible momentum and gives you your first real taste of financial peace of mind. This is Goal #1.

How to Calculate Your “Essential” Monthly Expenses

To figure out your long-term 3-6 month goal, you need to know your bare-bones budget. This isn’t what you normally spend; it’s what you would spend in a crisis. Grab a piece of paper or open a spreadsheet and add up the following:

- Housing: Rent or mortgage payment

- Utilities: Electricity, water, gas, internet

- Food: Groceries only (no restaurants or takeout)

- Transportation: Gas, public transit passes, car insurance

- Insurance: Health, life, and disability premiums

- Minimum Debt Payments: The minimum you must pay on any loans or credit cards

What to Exclude: Any expense you could cut in an emergency.

- Dining out and coffee shops

- Streaming subscriptions (Netflix, Spotify)

- Shopping for non-essentials (clothes, gadgets)

- Vacations and entertainment

To get an accurate number for your essential spending, look at your last two months of bank and credit card statements. Multiply that number by three to get your minimum long-term emergency fund goal.

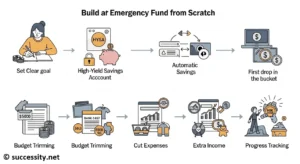

The 7-Step Plan to Build Your Emergency Fund from Scratch

Ready to go from $0 to financially secure? Follow these seven actionable steps.

Step 1 – Set Your First Goal ($500 or $1,000)

Forget the 3-6 month number for now. Your only focus is hitting that starter fund. Write it down and put it somewhere you can see it: “My goal is $1,000.” This makes your target real and keeps you focused. If $1,000 feels too big, start with $500. The key is to start.

Step 2 – Open a Separate, High-Yield Savings Account (HYSA)

This step is critical. Your emergency fund cannot live in your regular checking account. It’s too easy to accidentally spend it. You need to put it somewhere separate, following the “out of sight, out of mind” principle.

The best place for this is a High-Yield Savings Account (HYSA). These are online savings accounts that are FDIC-insured (meaning your money is safe) but pay interest rates that are often 10-20 times higher than traditional brick-and-mortar banks. Your money will grow faster, and it’s still easily accessible when you need it.

Step 3 – Automate Your Savings (“Pay Yourself First”)

This is the single most effective step you can take. Don’t rely on having leftover money at the end of the month. Instead, “pay yourself first” by setting up an automatic, recurring transfer from your checking account to your new HYSA.

Schedule the transfer for every payday. Start with an amount that feels painless, even if it’s just $10 or $25 per paycheck. The consistency is more important than the amount. You can, and should, increase it later. Automation does the work for you and builds your fund without you even thinking about it.

Step 4 – Find Your “First Drop in the Bucket”

To get a quick win and build momentum, find a lump sum to deposit right now. This is your seed money.

- Ideas for a quick deposit:

- Sell unused electronics, clothes, or furniture on Facebook Marketplace or Poshmark.

- Dedicate your next tax refund entirely to your fund.

- Use any work bonuses or cash gifts.

- Collect all the loose change in your house and car and deposit it.

Step 5 – Trim Your Budget and Redirect the Cash

Review your last bank statement and find 1-3 non-essential expenses you can cut, even just temporarily.

- Did you spend $40 on coffee?

- Do you have a $15/month streaming service you don’t watch?

- Could you pack your lunch three days a week to save $50?

Once you identify a saving, immediately go into your bank’s app and increase your automatic transfer by that exact amount. If you cancel a $15 subscription, set up a $15 monthly transfer. This directly converts your sacrifice into savings.

Step 6 – Get Creative with Extra Income

If you want to build your emergency fund fast, temporarily increasing your income is the quickest way.

- Ideas for extra income:

- Deliver food with DoorDash or Instacart on weekends.

- Offer your skills as a freelancer on sites like Upwork or Fiverr.

- Pick up overtime shifts at your job.

- Pet sit or walk dogs in your neighborhood using an app like Rover.

Funnel 100% of this extra income directly into your HYSA until you hit your $1,000 goal.

Step 7 – Track Your Progress and Celebrate Milestones

Watching your balance grow is incredibly motivating. Use a savings app or a simple chart on your fridge to track your progress. When you hit a milestone—like your first $250 or $500—celebrate! But do it with a free or low-cost reward, like a hike, a movie night at home, or cooking a special meal. This reinforces your positive behavior and keeps you in the game.

Where Is the Best Place to Keep Your Emergency Fund?

Choosing the right account is crucial. You need your money to be safe, accessible, and earning a little extra interest if possible.

The Best Option – High-Yield Savings Accounts (HYSAs)

- Pros: By far the best choice. They offer the highest interest rates for savings accounts, are FDIC insured up to $250,000, are liquid (you can usually get your money in 1-3 business days), and being separate from your checking account helps you avoid temptation.

Other Good Options – Money Market Accounts

- Pros: Very similar to HYSAs, offering competitive interest rates and FDIC insurance. They sometimes come with a debit card or check-writing privileges, which can add a layer of accessibility.

Places to AVOID for Your Emergency Fund

- Your primary checking account: It’s far too easy to spend the money on daily expenses. It needs to be separate.

- Investing in stocks or crypto: This is a huge mistake. The market is too volatile. Your fund could lose 20% of its value right when you need it most.

- Certificates of Deposit (CDs): Your money is locked up for a specific term. Withdrawing it early means you’ll pay a penalty, which defeats the purpose of having accessible cash.

When to Use Your Emergency Fund (A Simple Checklist)

You’ve worked hard to build your fund. Don’t sabotage your progress by using it for the wrong things.

✅ What IS a True Emergency?

- Job Loss: To cover essential bills while you find new work.

- Unexpected Medical or Dental Bills: For urgent procedures not covered by insurance.

- Urgent Home Repairs: A leaky roof, a broken furnace in winter, or a burst pipe.

- Essential Car Repairs: To fix your only mode of transportation to get to work.

- Emergency Travel: An unplanned trip for a family health crisis or funeral.

❌ What is NOT an Emergency?

- A flash sale on a new TV.

- A last-minute vacation deal.

- A down payment on a new car because you’re bored with your old one.

- Tickets to see your favorite band.

- Routine, planned expenses (like holiday gifts or annual car registration).

My Fund is Built! What’s Next?

Congratulations! Building a starter emergency fund is a massive accomplishment. Here’s what to do next.

- Replenish After Use: If you have to use your fund, your #1 financial priority becomes refilling it. Pause other savings goals (like retirement investing) and aggressively rebuild your fund back to its target level.

- Adjust as Life Changes: Your finances aren’t static. After you get a raise, get married, have a child, or buy a home, recalculate your 3-6 month expense goal and adjust your savings plan accordingly.

- Move to Other Goals: Once your starter fund is stable, you can confidently move on to your next financial goals, like aggressively paying down high-interest debt (credit cards, personal loans) or starting to invest for retirement.

Start Building Today

Building an emergency fund from scratch is a marathon, not a sprint. It’s about creating a new habit, one small deposit at a time. The anxiety you feel today about money doesn’t have to be your reality forever. By starting small, automating your savings, and staying consistent, you can build a financial foundation that provides true security and peace of mind.

Don’t wait for an emergency to force your hand. Open your separate savings account and schedule your first $10 transfer today. You can do this.

Frequently Asked Questions about emergency fund

How fast can I build a $1,000 emergency fund?

Saving $100/month will take 10 months, while saving $200/month takes 5. Aggressively cutting costs or adding a side hustle can get you there in just 1-2 months.

What if I have high-interest debt? Should I save or pay off debt first?

Always save your $1,000 starter fund first to prevent taking on more debt. Once that buffer is in place, you can switch your focus to aggressively attack the debt.

Is an emergency fund really necessary if I have a credit card?

Yes, absolutely. A credit card is a loan that creates high-interest debt, while an emergency fund is your own money that prevents debt and financial stress.

Can I use my emergency fund for a down payment on a house?

No. Your emergency fund is a safety net for unexpected crises. A down payment is a separate, planned savings goal that requires its own dedicated account.

What should I do after I use my emergency fund?

Your #1 priority is to pause other savings goals and immediately start rebuilding your fund. Direct all extra cash back into your savings until it’s full again.