5 Simple Steps to Start a Budget and Stick to It Successfully

Budgeting can feel overwhelming, but it’s a crucial skill for financial health and independence. Yet, starting a budget is only half the battle—the real challenge is sticking to it! In this guide, I’ll share a step-by-step process to create a budget that works for you and tips for sticking to it long-term. By the end, you’ll feel more confident managing your money and ready to tackle any financial goals you set. Let’s dive in!

Table of Contents

ToggleWhy You Should Start a Budget for Financial Stability

Budgeting may seem like a lot of effort, but it’s actually the secret weapon for building financial stability and freedom. Let’s face it: without a budget, it’s easy for money to slip through the cracks. You might find yourself wondering, “Where did it all go?” at the end of the month, only to realize that little purchases here and there added up fast. Creating and sticking to a budget changes this dynamic—it gives you control over your finances, helping you decide where each dollar should go based on your values and goals. But there’s even more to it!

Budgeting = Financial Freedom

Many people associate budgeting with restriction, but a budget is really a tool for financial freedom. By knowing your spending and saving patterns, you’re able to make intentional choices. Want to save up for a vacation? A budget lets you allocate funds for it without guilt or stress. Looking to buy a home? Budgeting can help you see where to cut back, save, and stay on track. And if you’re someone who feels overwhelmed by debt or uncertain about financial goals, budgeting provides clarity, showing you exactly how to move toward a more secure future.

Common Myths About Budgeting

Budgeting has picked up some unflattering myths over the years. One big misconception is that a budget means you can’t spend on anything fun. But budgeting isn’t about depriving yourself—it’s about choosing what really matters to you. For instance, if having a nice meal out once a week brings you joy, you can build that into your budget! Another myth is that budgeting is only for people who have “extra” money. But truthfully, budgeting is most helpful for anyone who’s looking to make the most out of what they have. No matter your income, having a plan in place is empowering and gives you a sense of control.

How Budgeting Reduces Stress and Improves Decision-Making

Think about all the decisions you make each day about money, from grabbing a coffee to paying bills. Without a plan, it’s easy to feel like every purchase is a stress point. But with a budget, you’ve already decided where your money goes. This makes everyday decisions simpler and less stressful because you’re following a plan you’ve created with your own goals in mind. For instance, when you budget for groceries, you don’t feel anxious about buying your weekly essentials. And knowing that you’ve saved for a specific purpose, like an emergency fund or a future goal, brings peace of mind.

In the end, budgeting helps you live life on your terms. It gives you a roadmap to follow, a plan that grows and adapts with you. Financial stability doesn’t happen overnight, but with budgeting, you’re creating the foundation for freedom, peace of mind, and the confidence that you’re in charge of your future.

Step 1: Set Clear Financial Goals

If budgeting is your roadmap, then financial goals are the destinations. Setting clear financial goals gives your budget purpose and direction. Without knowing what you’re working toward, it’s all too easy to feel like budgeting is just about restrictions or numbers on a page. But with concrete goals, each choice you make in your budget starts to feel meaningful—every dollar has a job, a purpose, and a reason to be there. This step will help you define those goals and start budgeting with intention.

Why Financial Goals Matter in Budgeting

Clear financial goals are crucial because they provide motivation. Think about it: saving money or cutting expenses just for the sake of it can feel draining and, honestly, unsustainable. But if you know you’re budgeting to save up for a down payment, build an emergency fund, or pay off debt, you’re much more likely to stick with it. Your goals act as reminders of why budgeting matters, especially on those tough days when it’s tempting to overspend or slack off.

Types of Financial Goals to Consider

When setting goals, it helps to think about both short-term and long-term objectives. Here’s a breakdown of each type:

- Short-Term Goals (0-12 months)

Short-term goals are the ones you can accomplish within a year. Examples might include saving for a holiday gift fund, creating a $1,000 emergency fund, or setting aside money for a weekend getaway. Short-term goals are motivating because they’re achievable in a shorter time frame, and they show you that budgeting can bring quick wins. - Medium-Term Goals (1-5 years)

Medium-term goals typically take a bit longer and require steady planning. These might include saving for a larger vacation, building a more robust emergency fund, or starting a fund for a specific purchase like a car. Medium-term goals encourage consistent budgeting habits and help you start building up larger amounts over time. - Long-Term Goals (5+ years)

Long-term goals are the big ones, like retirement savings, buying a home, or paying off a significant portion of debt. These goals are all about creating long-term financial stability and building wealth. It’s okay if these feel far off; the key is to include them in your budgeting strategy so you’re setting yourself up for the future.

Setting Your Own Financial Goals

When setting goals, try to make them SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, instead of a vague goal like “save more money,” go with something like, “Save $5,000 for an emergency fund within 12 months.” Specific goals give you something concrete to aim for and allow you to measure your progress along the way.

Here are a few steps to set your own goals:

- Define Your Priorities: Think about what you value most. Is it financial security, travel, education, or homeownership? Your goals should align with your values to feel meaningful.

- Write Them Down: Goals feel more real when you put them on paper or in a budgeting app. Keep them visible, so they serve as a constant reminder.

- Break Them Into Steps: For bigger goals, break them down into monthly or even weekly targets. Saving $5,000 in a year, for instance, becomes saving about $417 per month, making it feel more manageable.

Examples of Financial Goals to Inspire You

If you’re still unsure, here are some popular financial goals to consider:

- Build a $1,000 emergency fund

- Save $2,000 for a vacation next summer

- Pay off $3,000 in credit card debt within 12 months

- Save $10,000 for a down payment on a home within three years

- Put aside $500 for holiday shopping over the next six months

Having clear financial goals in place helps keep your budget on track and gives you a sense of purpose. Each time you look at your budget, you’re reminded of why you’re making these choices, and that motivation is what keeps you moving forward. So take a moment, set those goals, and let them be the guiding lights for your financial journey.

Step 2: Track Your Income and Expenses

Tracking your income and expenses is like putting on glasses when you’ve been squinting—you suddenly see your financial situation with complete clarity. This step is all about gathering the facts: how much money is coming in, where it’s going, and what adjustments you can make to align with your goals. Trust me, it’s eye-opening (and sometimes a little shocking). But once you know the numbers, you’ll feel more in control and ready to move forward.

Methods for Tracking Income and Expenses

There are plenty of ways to track your money, and the best method depends on your personality and lifestyle. Here are a few popular options:

- Budgeting Apps

Apps like Mint, YNAB (You Need a Budget), or PocketGuard make tracking easy and automated. They link directly to your bank accounts and credit cards, categorizing transactions for you. This is perfect if you’re tech-savvy or hate manual data entry. - Spreadsheets

Good old Excel or Google Sheets is another reliable choice. You can customize your spreadsheet to include income, fixed expenses, variable expenses, and savings. If you’re like me and enjoy having full control over the details, this method is super satisfying. - Manual Tracking

Pen and paper might sound old-school, but it works for some people! Writing things down gives you a tactile connection to your finances. You can also use a printed tracker or a budget planner notebook. This method is great if you like simplicity and don’t want to rely on tech.

No matter which method you choose, the key is consistency. Make it part of your routine, whether that’s at the end of each day or during a weekly financial check-in.

Benefits of Knowing Where Your Money Goes

I’ll be honest: the first time I tracked every expense, I was floored. I had no idea how much I was spending on coffee and takeout! But that clarity changed everything. Here’s how tracking your money can benefit you:

- Awareness of Spending Habits: When you track your expenses, you start to see patterns—both good and bad. You might realize you’re overspending in certain areas or discover small wins, like having extra room in your grocery budget.

- Opportunity to Cut Back: Once you know where your money is going, it’s easier to identify areas to cut back. For example, that streaming service you never use? Canceling it could save you $15 a month.

- Improved Financial Control: Tracking gives you a sense of control over your finances. Instead of feeling like money is disappearing, you’re telling it where to go.

- Easier Budget Adjustments: If you track consistently, adjusting your budget becomes much simpler. You’ll have real data to inform your decisions.

Tips for Staying Consistent with Tracking

Let’s be real—tracking income and expenses can feel like a chore at first. But the trick is to make it a habit that fits into your life. Here are a few tips to stay consistent:

- Set Reminders: Whether it’s a daily alert on your phone or a recurring calendar event, set aside time to update your tracker. Treat it like an appointment with your finances.

- Automate Whenever Possible: If you’re using apps, many of them can pull in transactions automatically. This saves time and reduces the chance of forgetting.

- Do Weekly Check-Ins: Instead of tracking every single day, carve out 10–15 minutes each week to review and update your records. Sunday evenings work well for many people—it’s a good way to prepare for the week ahead.

- Celebrate Small Wins: If you notice that you stayed within budget for groceries or saved a little more than expected, give yourself a pat on the back. Small victories keep you motivated!

- Make It Part of a Routine: Tie your tracking habit to something you already do. For example, while sipping your morning coffee or before starting your Netflix binge, spend a few minutes updating your budget.

Tracking your income and expenses is one of the most valuable habits you can build for financial success. It might feel tedious at first, but once you see how much insight it gives you into your spending, you’ll wonder how you ever managed without it. So grab an app, spreadsheet, or notebook, and start tracking—you’re on your way to smarter budgeting!

Step 3: Categorize and Prioritize Your Spending

Once you’ve tracked your income and expenses, the next step is to organize them into categories and decide what’s truly important. This is where budgeting becomes personal—you get to decide what matters most to you. Categorizing your spending not only helps you understand where your money goes but also makes it easier to spot opportunities to cut back or adjust.

Different Types of Budgeting Categories

Think of your expenses as falling into three main buckets: fixed expenses, variable expenses, and discretionary spending. Breaking your spending down like this helps you see the big picture and allocate your money more effectively.

- Fixed Expenses

These are the must-pays that stay consistent each month. Think rent or mortgage, car payments, insurance premiums, and utility bills. These expenses usually take priority because they keep the essentials in your life running smoothly. - Variable Expenses

These are necessary but can fluctuate from month to month. Examples include groceries, gas, and electricity if it’s not a fixed rate. Because these vary, they’re often where you can find some wiggle room in your budget. - Discretionary Spending

This is the “fun” category—things like dining out, streaming services, hobbies, and shopping for non-essentials. While it’s important to enjoy life, discretionary spending is often the first place to trim when you need to save more.

How to Prioritize Needs Over Wants

We all have moments where we convince ourselves that a “want” is a “need” (hello, those cute shoes or the latest gadget). But when budgeting, it’s important to clearly define your priorities. Here’s how to separate the must-haves from the nice-to-haves:

- Start with Your Needs

Needs are things you truly can’t do without, like housing, food, transportation, and healthcare. These should be the first items covered in your budget. Ask yourself: “If I lost my job tomorrow, what expenses would I absolutely need to keep paying?” - Define Your Wants

Wants are everything else—the things that make life more enjoyable but aren’t necessary for survival. This could include going out to eat, subscription boxes, or upgrading to the newest phone. Be honest about what you truly need versus what’s just adding a little extra joy. - Use the 50/30/20 Rule as a Guide

If you’re unsure how to balance your budget, the 50/30/20 rule can help:- 50% for needs

- 30% for wants

- 20% for savings or debt repayment

While it’s not a one-size-fits-all formula, it provides a helpful starting point to prioritize your spending.

Tips for Trimming Non-Essential Spending

Cutting back on wants doesn’t mean giving them up entirely—it’s about being intentional. Here are some ways to trim the fat in your discretionary spending without feeling deprived:

- Identify Subscription Overlap

Do you really need Netflix, Hulu, Disney+, AND Amazon Prime? Evaluate your subscriptions and cancel the ones you’re not using regularly. - Limit Dining Out

Eating out is one of the easiest areas to overspend. Try cooking more at home or setting a specific “eating out” budget for the month. - Shop Smart

Before making a purchase, ask yourself: “Do I truly need this right now?” Waiting 24 hours before buying something can help curb impulse spending. - Embrace Free Entertainment

Swap pricey outings for free or low-cost activities like picnics, hikes, or library visits. Fun doesn’t always have to come with a price tag. - Set Spending Challenges

Challenge yourself to spend nothing on non-essentials for a week or even a month. It can be a fun (and eye-opening) way to reset your spending habits.

Bonus Tip: Use Visuals to Prioritize

A visual tool like a pie chart or bar graph of your spending categories can really drive home where your money is going. Sometimes seeing that big slice labeled “discretionary” can inspire you to make more thoughtful choices.

Categorizing and prioritizing your spending is where budgeting starts to feel intentional. It’s no longer about just tracking numbers—it’s about aligning your money with your goals and values. Once you’ve trimmed the excess and focused on what truly matters, you’ll find budgeting becomes less stressful and more empowering.

Step 4: Choose a Budgeting Method That Fits Your Lifestyle

There’s no one-size-fits-all approach to budgeting—what works for one person might feel completely unmanageable for another. That’s why choosing a budgeting method that aligns with your lifestyle is so important. Whether you like detailed planning or prefer something low-maintenance, there’s a method out there for you. Here’s a rundown of popular budgeting styles, their pros and cons, and tips for finding the one that fits your needs.

Overview of Popular Budgeting Methods

- 50/30/20 Rule

This method divides your income into three categories:- 50% for needs (essentials like housing, food, and transportation)

- 30% for wants (entertainment, dining out, and other non-essentials)

- 20% for savings or debt repayment

It’s simple, straightforward, and great for those who don’t want to track every dollar.

- Envelope Method

With this cash-based method, you allocate a set amount of money to different spending categories, placing the cash in labeled envelopes. For example, one envelope might be for groceries, another for entertainment. Once the cash is gone, you can’t spend more in that category until the next budgeting period.It’s highly effective for controlling overspending and staying disciplined, but it requires commitment and works best for those comfortable using cash instead of cards. - Zero-Based Budgeting

This method assigns every dollar of your income to a specific purpose, so your income minus expenses equals zero. Each month, you start fresh, giving your money clear jobs, from bills to savings to discretionary spending.Zero-based budgeting is great for control freaks (like me!) who love tracking every detail, but it can be time-consuming to maintain. - Pay-Yourself-First Method

This approach prioritizes savings by treating it like a non-negotiable expense. You “pay yourself” by setting aside money for savings or investments first, then allocate what’s left to other spending.It’s perfect for building savings quickly but may require discipline to live on the remaining income. - Percentage-Based Budgeting

Similar to the 50/30/20 rule, this method lets you choose custom percentages for your spending, saving, and investing goals. It’s flexible and great for those who want a mix of structure and personalization.

Pros and Cons of Each Method

| Budgeting Method | Pros | Cons |

|---|---|---|

| 50/30/20 Rule | Easy to follow; minimal effort required | Lacks precision; may not suit tight budgets |

| Envelope Method | Limits overspending; highly visual | Requires cash; less convenient in digital age |

| Zero-Based Budgeting | Complete control; highly detailed | Time-consuming; can feel rigid |

| Pay-Yourself-First | Savings-focused; encourages long-term growth | May lead to overspending with leftover funds |

| Percentage-Based | Flexible; customizable | Requires careful percentage selection |

How to Pick a Budgeting Style That’s Realistic for You

Choosing the right budgeting method depends on your personality, lifestyle, and financial goals. Here are some tips to help you decide:

- Reflect on Your Goals

If building savings is your top priority, a savings-first method like pay-yourself-first might work best. If you want simplicity, go with the 50/30/20 rule. - Assess Your Spending Habits

Are you prone to overspending in specific categories? The envelope method could be a game-changer. If you like knowing where every dollar goes, you might love zero-based budgeting. - Be Honest About Your Lifestyle

If you’re always on the go, a cash-only system might feel inconvenient. On the other hand, a digital app or percentage-based method might fit seamlessly into your routine. - Try Before You Commit

Experiment with a method for a month or two to see how it feels. You can always adjust or switch methods if it doesn’t feel right. - Combine Methods

Don’t be afraid to mix and match! For example, you might use the 50/30/20 rule as a broad framework while applying zero-based budgeting for specific goals like saving for a vacation.

Finding What Works for You

There’s no right or wrong way to budget—it’s all about what feels realistic and sustainable. The best budgeting method is the one you can stick to over time, even when life throws curveballs. Start simple, make adjustments as needed, and remember: the goal is progress, not perfection.

Step 5: Adjust and Optimize as Needed

Creating a budget is a fantastic first step, but it’s not a “set it and forget it” kind of thing. Life changes—unexpected expenses pop up, your income fluctuates, or your priorities shift—and your budget needs to keep up. Adjusting and optimizing your budget ensures it stays relevant and effective. Trust me, tweaking your budget over time isn’t failure; it’s just part of the process.

Signs Your Budget Needs an Adjustment

Here are some red flags that your budget might need a tune-up:

- You’re Consistently Overspending in Certain Categories

If you keep blowing past your budget for groceries or entertainment, it’s time to reassess. Maybe prices have increased, or your lifestyle has changed. Either way, adjust those numbers to better reflect reality. - You’re Struggling to Stick to It

A budget that feels too restrictive is hard to maintain. If you’re constantly tempted to ignore it, loosen the reins a bit and allow yourself more flexibility. - You’re Not Hitting Your Financial Goals

If your savings aren’t growing or your debt repayment feels stagnant, it’s time to revisit your plan. Small changes, like cutting back on wants or increasing savings contributions, can make a big difference. - Your Income or Expenses Change

A raise at work, job loss, or new expenses (hello, car repairs!) can throw off your budget. Adjusting immediately ensures you stay on track. - You Feel Overwhelmed

If budgeting has become stressful or overly complicated, simplify it. An effective budget is one you can manage without constant frustration.

When and How to Reassess Your Goals and Spending

Even if everything seems to be going well, regularly reassessing your budget is a smart move. Here’s when and how to do it:

- Review Monthly

Set aside time at the end of each month to look at how you did. Did you stay within your limits? Are you closer to your goals? A monthly check-in lets you catch issues early. - Revisit Goals Every 6–12 Months

Your financial goals may evolve over time. Maybe you’ve paid off a big debt and want to focus on investing, or your dream vacation is now within reach. Realign your budget to reflect your current priorities. - Adjust for Major Life Events

Got a promotion? Just had a baby? Moving to a new city? Big changes call for a budget overhaul to accommodate new income, expenses, or priorities. - Use Tracking Tools

Apps or spreadsheets can help you spot trends over time. If you notice, for example, that utility costs are climbing each month, you can adjust your budget to account for it. - Ask Yourself What’s Working

Don’t just focus on what’s going wrong. Identify what’s going well and double down on those areas. Are you excelling at meal prepping to save on groceries? Awesome—keep it up!

Tips for Keeping Your Budget Adaptable and Flexible

Life is unpredictable, so your budget needs some built-in flexibility. Here’s how to make sure it can roll with the punches:

- Build an Emergency Fund

This is your safety net for unexpected expenses. Having 3–6 months of living expenses saved can prevent financial stress when surprises arise. - Create a “Miscellaneous” Category

Set aside a small chunk of your budget for unplanned expenses. Whether it’s a last-minute birthday gift or a forgotten bill, this cushion can save you from scrambling. - Focus on Percentages, Not Exact Numbers

If your income varies (like with freelancing or commission-based work), base your budget on percentages instead of fixed amounts. For example, allocate 50% for needs, 30% for wants, and 20% for savings. - Allow for Small Splurges

A rigid budget can feel suffocating. Build in a little “fun money” to spend guilt-free—it keeps you motivated to stick with the rest of your plan. - Simplify When Needed

If your budget has too many categories, consider consolidating. For example, instead of separate “Netflix” and “Spotify” categories, combine them into “Subscriptions.” - Embrace Imperfection

No budget is flawless. Some months you’ll overspend, and that’s okay! The key is to learn from those moments and adjust moving forward.

Why Adjusting Your Budget Matters

Think of your budget as a living, breathing document. By adjusting it regularly, you’re ensuring it grows with you, aligns with your goals, and supports your lifestyle. Flexibility is what makes budgeting sustainable over the long term. Keep optimizing, and you’ll find it’s less about restricting your money and more about empowering yourself to make confident financial decisions.

Strategies to Stick to Your Budget

Creating a budget is one thing—sticking to it is a whole other ball game. It’s like starting a new workout routine: the first week feels great, but staying consistent takes effort. The good news? With a few smart strategies, you can make sticking to your budget a natural part of your routine, even when motivation wanes.

Setting Reminders and Tracking Progress

Out of sight often means out of mind, and that’s the last thing you want for your budget. Regular reminders and tracking progress help keep you engaged and on track.

- Set Calendar Alerts

Schedule weekly or bi-weekly check-ins on your phone or calendar to review your spending and make adjustments. Seeing that reminder pop up can be the nudge you need. - Use Budgeting Apps

Apps like Mint, YNAB (You Need a Budget), or PocketGuard can automatically track your income, expenses, and savings goals. They send notifications when you’re nearing your limits, making it easy to stay aware. - Track Progress Visually

Use a chart, graph, or even a thermometer-style tracker (like those fundraising visuals) to monitor your progress toward financial goals. Color it in as you get closer—seeing the visual progress can be surprisingly motivating. - Daily Check-Ins

Spend five minutes at the end of each day reviewing your spending. It’s a simple habit that keeps you mindful without feeling overwhelming.

Accountability Tools

Having someone—or something—keep you accountable makes a huge difference. When you know you’ll have to answer to someone, you’re more likely to stick to your plan.

- Find an Accountability Partner

This could be your spouse, a friend, or a family member. Share your budgeting goals and schedule regular check-ins to update each other on progress. - Join a Financial Community

Online forums, Facebook groups, or local budgeting meetups can offer support and advice. Sharing wins (and challenges) with like-minded people makes the process more enjoyable. - Use Apps with Accountability Features

Some apps allow you to share progress with partners or friends. For example, Splitwise is great for tracking shared expenses, while apps like Goodbudget let you share budgets across users. - Create Visual Reminders

Put sticky notes on your fridge or mirrors with affirmations like, “Stick to the plan!” or reminders of your savings goals (e.g., “Hawaii 2025!”).

Ways to Handle Budget Fatigue and Stay Motivated

Let’s face it: even the best plans can feel draining after a while. Budget fatigue is real, but you can combat it with these tips:

- Celebrate Small Wins

Paid off a credit card? Saved $100 more than last month? Treat yourself—but within the budget. Small rewards reinforce your good habits. - Focus on Your “Why”

Remind yourself why you’re budgeting. Is it to pay off debt? Save for a dream vacation? Retire early? Keeping that goal front and center makes the sacrifices feel worth it. - Switch Things Up

If your current budget feels stale, try a new method for a month (like moving from zero-based budgeting to the envelope method). A fresh approach can reignite your interest. - Give Yourself Grace

Nobody sticks to a budget 100% of the time, and that’s okay. If you slip up, don’t beat yourself up—just get back on track. Progress is what counts, not perfection. - Make It a Game

Challenge yourself to spend less than $100 on groceries one week or save $50 extra this month. Turning budgeting into a challenge can make it more fun. - Keep Your Budget Flexible

Life changes, and your budget should too. Allow room for adjustments when needed—it’s better to modify your budget than to abandon it entirely. - Stay Inspired

Follow financial blogs, podcasts, or YouTubers who share their budgeting journeys. Seeing others succeed can keep you motivated.

Why Sticking to Your Budget Matters

At its core, sticking to a budget is about building the habits that will lead to long-term financial success. It’s not always easy, but the payoff—less stress, more savings, and the freedom to achieve your goals—is worth it. Remember, every step you take is a step closer to financial security and independence. Keep at it, and don’t forget to celebrate the journey!

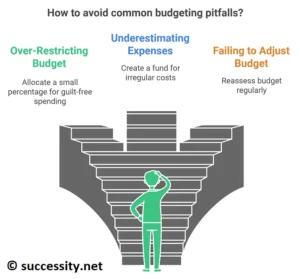

Common Budgeting Pitfalls and How to Avoid Them

Budgeting isn’t just about crunching numbers—it’s also about avoiding the sneaky traps that can derail even the best-laid plans. From underestimating costs to being too strict, many people make avoidable mistakes. Luckily, I’ve learned (sometimes the hard way!) how to steer clear of these pitfalls. Let’s talk about common budgeting blunders and how to keep your budget in tip-top shape.

Common Budgeting Mistakes

- Over-Restricting Your Budget

- Being too strict can backfire. Cutting out all “wants” like coffee runs or movie nights might feel noble at first, but it’s not sustainable. Life is meant to be enjoyed, so build in some wiggle room for fun.

- How to Avoid It: Allocate a small percentage of your budget (say 5–10%) for guilt-free spending. Label it “fun money” or “treat fund.”

- Underestimating Expenses

- It’s easy to forget about irregular costs like birthday gifts, car maintenance, or holiday expenses. These surprises can throw off your entire budget.

- How to Avoid It: Review your past spending to identify overlooked categories. Create a “miscellaneous” or “irregular expenses” fund to cover them.

- Failing to Adjust Your Budget

- Life changes—whether it’s a new job, higher bills, or different goals—but many people stick to an outdated budget.

- How to Avoid It: Reassess your budget regularly (monthly or quarterly) to ensure it matches your current reality.

- Neglecting an Emergency Fund

- Without a safety net, unexpected expenses like medical bills or car repairs can blow up your budget.

- How to Avoid It: Prioritize building an emergency fund with 3–6 months’ worth of expenses. Start small, even $10–$20 a week, and grow it over time.

- Tracking Inconsistently

- Losing track of spending leads to overspending or missed opportunities to save.

- How to Avoid It: Use budgeting apps, set reminders for regular check-ins, or spend five minutes a day reviewing your transactions.

- Setting Unrealistic Goals

- If your goals are too ambitious, you’re setting yourself up for frustration. For example, trying to save 50% of your income when you’re barely covering expenses can feel demoralizing.

- How to Avoid It: Start small and scale up. Focus on realistic, attainable goals to build confidence and momentum.

How to Prepare for Unexpected Expenses

Life is unpredictable, but your budget doesn’t have to suffer when surprises arise. Here’s how to stay ready:

- Create an Emergency Fund

- This is your first line of defense. Even a modest emergency fund can help you handle unexpected costs without derailing your budget.

- Use Sinking Funds

- Sinking funds are mini savings accounts for specific expenses. For example, set aside money each month for annual car registration or holiday shopping.

- Stay Insured

- Health, auto, and renters/home insurance can save you from catastrophic financial losses. Review your policies to ensure you’re adequately covered.

- Budget for the Unpredictable

- Include a “buffer” in your budget—about 5–10% of your monthly income—to handle surprise costs like a broken appliance or last-minute travel.

Tips for Staying Realistic and Avoiding Burnout

- Set Flexible Goals

- Your budget should evolve with you. If saving for a vacation feels too tight right now, scale back and extend the timeline.

- Automate What You Can

- Set up automatic transfers for savings, bills, and investments. Automation reduces decision fatigue and ensures you stick to your plan without constant effort.

- Reward Yourself

- Budgeting isn’t about deprivation—it’s about balance. Treat yourself occasionally when you hit milestones, like sticking to your budget for three months straight.

- Focus on Progress, Not Perfection

- Nobody sticks to their budget perfectly all the time. What matters is that you’re consistently moving toward your goals, even if it’s slower than you’d like.

- Revisit Your “Why”

- Keep your motivation front and center. Whether it’s becoming debt-free, saving for a home, or retiring early, reminding yourself of the bigger picture can keep you going.

- Add Variety to Your Budget Routine

- If reviewing your budget feels monotonous, switch things up. Use different apps, try a new budgeting method, or make it a game (e.g., challenge yourself to save $50 more than last month).

Why Avoiding Pitfalls Matters

Avoiding budgeting mistakes doesn’t mean you’ll never slip up—it just means you’ll have the tools to recover quickly. By preparing for the unexpected, staying realistic, and avoiding burnout, you’ll build a budget that works for you, not against you. Budgeting is about creating a roadmap for your financial journey, and with a little practice, you’ll navigate it like a pro!

The Benefits of Sticking to Your Budget Long-Term

Sticking to your budget might not always feel glamorous, but trust me, the long-term rewards are absolutely worth it. Imagine waking up stress-free, knowing your bills are paid, your savings are growing, and you have a plan for the future. Consistent budgeting isn’t just a financial tool—it’s a lifestyle upgrade. Let’s dive into the perks of staying committed to your budget and how it can transform your life.

Positive Impacts of Consistent Budgeting

- Increased Savings

- When you stick to a budget, every dollar has a purpose. Over time, those small, intentional choices add up to big savings.

- Example: Skipping a $5 coffee every weekday saves $100 a month—that’s $1,200 a year! Redirect that to an emergency fund, and you’ve got a safety net in no time.

- Reduced Stress

- Financial uncertainty is a major stressor, but budgeting brings clarity and control. Knowing exactly where your money is going removes the guesswork.

- Personal Note: I used to panic every time a bill came due. Once I started budgeting, I knew what was covered and when—no more late fees, no more anxiety.

- Freedom to Enjoy Life

- With a budget, you can prioritize spending on what truly matters to you. Whether it’s travel, hobbies, or family time, budgeting helps you fund your passions guilt-free.

- Improved Decision-Making

- Consistent budgeting teaches you to evaluate purchases and distinguish between needs and wants. Over time, this habit becomes second nature.

- Debt-Free Living

- Budgeting helps you allocate money toward debt repayment while avoiding new debt. Imagine living without monthly credit card bills—that’s financial freedom!

How Budgeting Builds Habits for Financial Success

- Discipline and Patience

- Budgeting forces you to think long-term, delaying instant gratification for future rewards. This habit translates to other areas of life, like career planning or health goals.

- Goal-Setting Skills

- Budgeting helps you define clear, actionable goals, whether it’s saving for a vacation or building an emergency fund. These skills carry over to achieving non-financial milestones.

- Awareness and Accountability

- Tracking income and expenses makes you mindful of your financial behavior. Over time, this awareness becomes second nature, helping you avoid wasteful habits.

- Confidence with Money

- Managing your budget successfully builds financial confidence. You’ll feel empowered to make decisions like investing, starting a business, or negotiating a raise.

Success Stories to Inspire You

- The Debt-Free Journey

- A friend of mine was drowning in $20,000 of credit card debt. She created a zero-based budget, focused on paying off her smallest debts first (the snowball method), and made extra payments whenever possible. Three years later, she’s debt-free and saving for her first home.

- Vacation Without Guilt

- I once saved for a trip to Italy by setting aside $200 a month. By the time the trip rolled around, all my expenses were paid upfront, and I didn’t have to worry about racking up debt.

- Building an Emergency Fund

- A couple I know started small, saving just $50 a month. After two years, they had over $1,200 set aside—enough to cover unexpected medical expenses without dipping into credit.

Why Long-Term Budgeting Matters

Sticking to your budget is like planting seeds: the effort you put in now grows into financial stability, freedom, and peace of mind. Over time, you’ll realize it’s not about restriction—it’s about empowering yourself to live the life you want, without financial stress holding you back.

Every success story starts with a single step. So whether you’re saving for a dream, paying off debt, or just trying to stay afloat, remember: consistency is key. Stick to your budget, and you’ll see the benefits unfold in ways you never imagined. Keep going—you’ve got this!

Conclusion

Starting a budget is a significant first step, but sticking to it is where the real growth happens. With the right tools, methods, and mindset, you can turn budgeting into a habit that helps you reach your financial dreams. Ready to get started? Begin with small steps and remember: every little effort counts. Let us know your budgeting tips or challenges in the comments!

Your Guide to Starting a Budget: FAQs

Q1: How can I make budgeting easier?

Start with realistic goals and pick a simple budgeting method, like the 50/30/20 rule, that fits your lifestyle. Track spending weekly instead of daily to avoid burnout, and use apps to automate parts of the process.

Q2: What if I keep breaking my budget?

If overspending is a pattern, create an “unexpected expenses” category and add a buffer of 5–10% of your income to cover surprises. Track your spending to find problem areas—like dining out or impulse buys—and adjust accordingly.

Q3: How do I stay motivated to stick to a budget?

Celebrate small wins, like staying under your grocery budget or saving an extra $50. Keep your “why” front and center—whether it’s paying off debt, saving for a dream vacation, or achieving financial independence.

Q4: What should I do if I have irregular income?

For irregular income, focus on budgeting with your average monthly earnings. Prioritize fixed expenses and essential categories first, and direct extra income toward savings or variable expenses when it comes in.

Q5: How can I handle budgeting as a couple?

Start by discussing financial goals together to align your priorities. Choose a shared budgeting method, like a joint app or spreadsheet, and hold regular “money dates” to review progress and address concerns as a team.

Q6: Is it okay to adjust my budget?

Absolutely! Your budget should be flexible to accommodate life changes, like a new job or unexpected expenses. Review it monthly or quarterly and make adjustments as needed to keep it realistic and effective.

About the Author

Sophia

Administrator

Hi, I’m Sophia. I believe success isn't just about wealth - it's about freedom. After a decade in corporate leadership, I founded Successity to cut through the noise. Here, I share actionable strategies to help you master your money, accelerate your career, and build a life you actually love. Let’s level up together.